British economist Edmund Burke summarized Pakistan and its economy comprehensively when he said, “If we command our wealth, we shall be rich and free; if our wealth commands us, we are poor indeed.”

The external debt of Pakistan accounts for up to $130.1 billion. Compared to other countries, it is smaller, but multiple factors such as debt-to-GDP (gross domestic product) ratio, creditworthiness, finance structures, political stability, and governance place Pakistan in a precarious position. Moreover, other economic factors such as foreign reserves, GDP, balance of payments, trade balance, unemployment rate, and per capita income signify a deteriorating economic outlook for development in Pakistan.

Impact of Covid-19 on the Economy of Pakistan

The ripples caused by the onslaught of the pandemic upon the world in terms of the economy are still visible today. A decade earlier, the global economic growth rate was predicted to be 3.9%. However, this trend did not carry on as the global growth rate in 2022 was at 3.5%, plunging to 3% in 2023, and expected to fall further to 2.9% in 2024.

Many advanced economies have been impacted by Covid-19. Growth rates of such countries have either halted or backtracked exponentially, with a 2.6% growth rate in 2022, plummeting to 1.5% in 2023, and predicted to sink further to 1.4% in 2024 by the International Monetary Fund (IMF).

Nevertheless, emerging markets have shown resilience as their growth rates declined by only one decimal point, from 4.1% to 4%. This is because emerging markets have had more economic space. Astonishingly African markets have shown great economic thrust, with countries like Niger, Senegal, Rwanda, and Ethiopia having growth rates of 9.6%, 9.4%, 7.9%, and 6% respectively.

In our immediate neighborhood, countries like India, Bangladesh, Iran, and China have had respectable growth (considering that the aggregate global economy has contracted) of 6.33%, 6.9%, 3.8%, and 5.4%, respectively. Except for Afghanistan (recovering from a negative growth rate of 20% in 2022 to a negative 3% at the end of 2023) and Sri Lanka (expected to end the year with 2.3%), as they’ve both suffered additional perils, such as the likes of war and destructive political instability.

Pakistan, too, is a developing or emerging market; it has yet to show the prospects other similar markets have, especially in 2023. Indisputably, the year 2022 was promising for the economy as GDP development was at a decent 6.9% with indications to increase further before the country was plunged into another political debacle and its growth rate was slashed to 0.29%. Currently, the state ended 2023 at a negative 0.5%.

Many argue that the GDP growth rate is not the only factor that must be analyzed to suggest that a country is prospering conclusively. Although it is correct, if the same economic policy responsible for such significant growth were to be coupled with consistency and versatile economic frameworks, other microeconomic indicators for Pakistan would also start showing positive prospects for the citizens through the trickle-down effect.

Pakistan’s economy relies 20% on the agriculture sector, 50% on the services sector, and 30% on the industrial sector. Manifold efforts and policies have been executed to bolster all of these. Economic policies since 1950 have been aimed at converting Pakistan from an agro-based economy to a more industrialized economy.

5-Year Plans

The “5-year plans” were adopted in the 1950s, with Liaquat Ali Khan promulgating this initiative. Considering the USSR’s economic growth in the 1950s, implementing a 5-year plan was a sagacious step.

1st Plan (1950-1955)

The Pakistan Industrial Development Corporation (PIDC) was formed in 1952, but the 1st plan failed due to insufficient availability of skilled labor.

2nd Plan (1960-1965)

It was resurrected in 1955, and again, industrialization was the main goal, but political instability hindered it from achieving its full potential. In the 2nd plan, under Ayub Khan from 1960 to 1965, the industrial and agro-economy was targeted to achieve subsistence. Some attention was also given to achieving an increment of 20% in the national income.

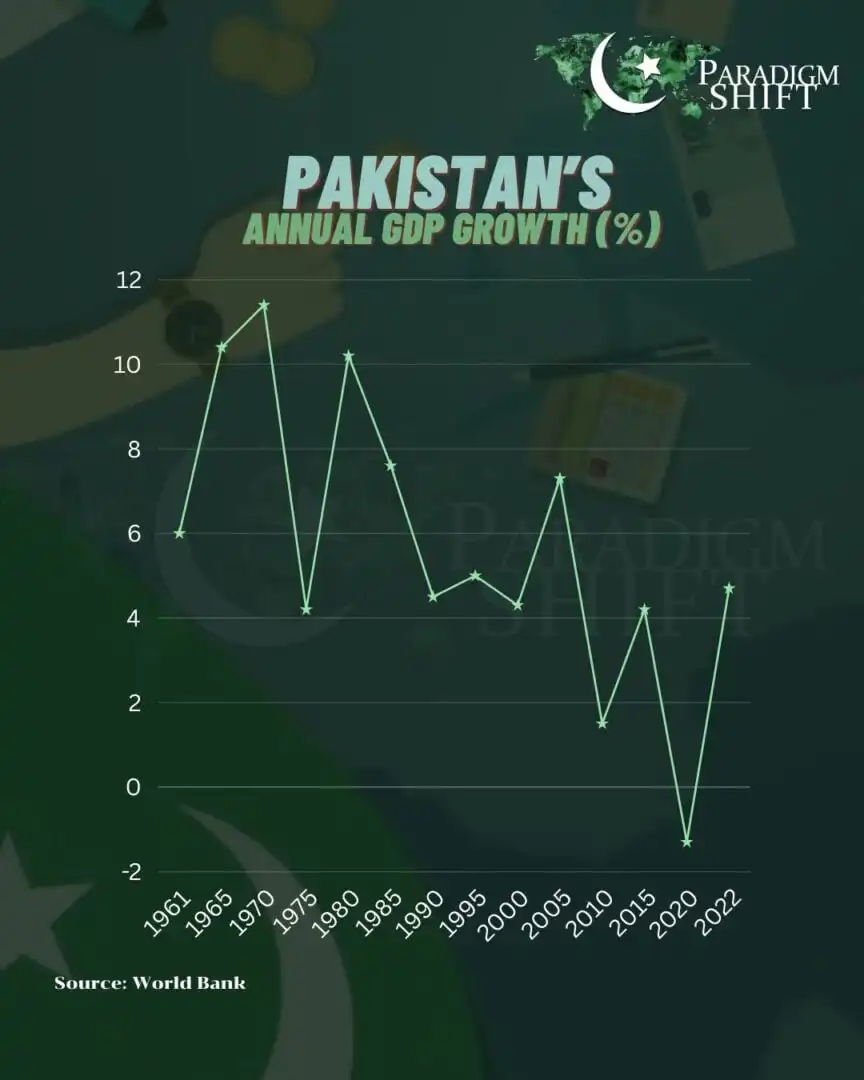

Many impediments distorted Pakistan’s 2nd 5-year plan, such as the Bajaur campaign from 1960 to 1961, the political putsch in Baluchistan, and the 1965 war. But still, by the end of 1965, Pakistan had a GDP growth rate of a staggering 10.42%, with an average five-year growth of 5.2%.

3rd Plan (1965-1970)

The 3rd plan followed with a targeted 6.5% growth potential. It stated that it would learn from the past 15 years and target accelerated growth for the coming 2 decades. As far as the industry was concerned, it followed the same pattern as it did during the 2nd plan, but this time around there was an emphasized enhancement of agriculture. The plan concluded on a high note, with the GDP growth rate nudging at 11.35%.

4th Plan (1970-1975)

The 4th plan was chiefly put into play under Bhutto. It mainly focused on the nationalization of various economic institutes, from banking to mass production and agriculture. It aimed to make the economy self-reliant and supported the synthesis of economic growth and social justice. However, this plan came to be amidst a catastrophic time which included the fall of Dhaka and severe internal political upheaval. For the first time, a 5-year plan concluded at a GDP growth rate below 5%, at 4.21%.

64% of the population is younger than the age of 30. In the 4th plan, some attention was paid to the development of human resources and the population’s education (primarily youth). It was planned that enrollment in vocational training schools would be increased by 280%, concurrently making education till grade 5, universal.

5th Plan (1978-1983)

The consecutive implementation of the 5-year plans ended in 1975. They were rejuvenated in 1978 with the 5th plan. It emphasized the completion of deferred projects. Additionally, it prioritized agriculture and the incorporation of modern farming methods. In the industrial ambit, it encouraged the completion of the Karachi steel mill and other cement and fertilizer plants and factories. Furthermore, it was also focused on the reversal of nationalization that took place during the 4th plan. At the close of 1983, the GDP growth was at 6.8%.

6th Plan (1983-1988)

The 6th plan followed up with an additional goal, which focused on human resource development and amelioration of the energy sector’s infrastructure. It also emphasized addressing regional imbalances. This 5-year plan focused on establishing an industry capable of making ‘capital goods’ such as tractors. At the end of 1988, it had a GDP growth rate of 7.6%.

7th Plan (1988-1993)

The 7th plan tried to stimulate private investment and followed pretty much the same outline of the plans implemented prior to it. Until the 1990s, Pakistan made significant economy-centered policies embodying the 5-year plans. Nevertheless, we have seen a decline in the formation of palpable policies that showed some cogent intent.

Musharraf introduced the medium-term development framework replacing the 5-year plans. During the premiership of Musharraf, no significant ‘sustainable’ growth existed. Certain aspects did show positive signs such as the investment-to-GDP ratio hitting 23%, one of the highest figures ever. Some structural reforms were introduced in the tax sector, such as value-added tax, automation, and reorganization of the taxing body. His economic efforts reduced the poverty headcount from 34% to 15%, but this was limited to certain regions and instigated further regional disparity.

All in all, economic indicators were showing convivial signs, but the solutions were myopic and unsustainable. This is exactly why, after 2004, GDP growth started declining annually, from a 7.55% high in 2004 to an almost rock bottom of 1.7% in 2008 (the reason being economic calamities coupled with multiple other perennial factors). Previously, most policies aimed at achieving ‘self-generating’ economic growth. This was not the case with Musharraf’s economy.

PPP Takes Over

By 2008, the entire world was undergoing an economic recession. Commodity prices surged by 50%, and oil prices almost doubled. Pakistan’s reserves stood at $13.3 billion but were rapidly deteriorating because of the government’s subsidies for lower wheat, electricity, and oil prices. Amid the crisis, many foreign investors were losing confidence in the domestic economy and started withdrawing from Pakistan’s stock market. Local investors started selling too, which caused a 20% drop in the market.

The Pakistan Peoples Party (PPP) took over after Musharraf. The economy was dilapidated due to the virulent shocks of the 2008 economic downturn. However, this was not the end of the disastrous pummeling that Pakistan’s economy was to undertake.

Due to the floods in 2010, the economy again suffered a gargantuan blow of $43 billion in damages. Pakistan did receive aid, but it was an infinitesimal $1.3 billion. This economic backlash forced the PPP to seek fiscal help from friendly countries and borrow loans from the IMF. Certain trade agreements were concluded with Saudi Arabia and a package worth $11.3 billion was finalized with the IMF.

Pakistan received $7.4 billion from the IMF; the institution concurrently forced Pakistan to take up several economic reforms. These mainly targeted the increment of the tax base and further privatization of the economy. Despite the loans and all the efforts made, the Pakistani economy failed to recover.

Foreign direct investment (FDI) was limited, growth rates were slashed, and regardless of the IMF’s impetus for increasing the tax base, the tax-to-GDP ratio was 9% in FY2013-14. During the same period, India was at 17.2%. According to the World Bank, a 15%+ tax-to-GDP ratio is considered viable for economic growth.

PML-N Succeeds PPP

During PPP’s premiership, there was no definite plan to uplift the economy. Similarly, no such efforts were made during the reign of Pakistan Muslim League Nawaz (PMLN). Growth rates were at 6.19%. IMF loans and CPEC (China-Pakistan Economic Corridor) majorly supported the economy. CPEC, at its full capacity, is to add a 2%—2.5% growth rate to the economy. This will not be sufficient to sustain the economy of 240 million people.

Furthermore, several sectors of the economy were neglected due to which exports fell drastically. The agricultural sector in Pakistan had a negative 0.19% growth rate. The cherry on top of PMLN’s ruthless massacre of the economy was that cotton was imported from India duty-free, ultimately sending our cotton farmers on a run for their money. This engendered the reduction of Pakistan’s cotton bales being harvested from an average of 12 million to only 9.9 million.

Still, much attention was given to infrastructure development. The entire country was connected through a network of roads. Additionally, good steps were taken to improve the country’s educational facilities. Raising the education budget from 2.6% of the GDP to 4% by 2018 was one of the commitments taken to bolster educational development. Enrollment in schools was improved by 80% whilst 22 schools in Islamabad were revamped by March 2016.

PTI Comes Forward

Lastly, we come to the government of Pakistan Tehreek-e-Insaf (PTI). The PTI government tried to reduce the trade deficit, replenish the foreign reserves, and tackle the pandemic effectively. Since 2008, it has been the only government to maintain a growth rate of over 6% for two consecutive years. Pakistan’s foreign exchange reserves hit an all-time high of $27 billion in 2021.

The agricultural sector recorded a growth of 4.3% while crop output was at 8.2%. This agricultural growth was attributed to the National Agriculture Emergency Program. Similarly, the government hoped to improve the irrigation set-up as well. The PTI government was targeting a growth rate of 7% in the subsequent year; nevertheless, its tenure was short-circuited.

What Next?

Having had an overview of the entire economic picture through the years, we can see that up until the 5-year plans, there was proper intent to put the economy on the right track. This intent starts to diminish after the 5th 5-year plan. Policies, reforms, and a proper road map for improving the economy are paramount. In our immediate neighborhood, India established proper policies after the economic crisis it faced in 1991. It aimed at the liberalization, privatization, and globalization of its economy.

The Indian Prime Minister of that time, Narasimha Rao, introduced multiple policies to restructure the economy and based them upon the three above-mentioned principles. However, India did not just indulge in such frameworks one time and then allow the economy to float on its own. It revisits its economic policies on an average 10-year period. It is not just India; rather every successful economy, including China or other G20 member countries. They continuously introduce prudent economic policies to make sure their economy is robust enough to face contemporary and future challenges.

Najy Benhassine, the country director for Pakistan in the World Bank, has emphasized that Pakistan needs careful economic management and ‘deep structural’ reforms. Furthermore, Pakistan needs to work on its human resource management for real growth. Currently, our literacy rate is 59%, and only 3.6% of the population holds a bachelor’s degree. The People’s Republic of China, on the other hand, undertook noteworthy steps to enhance its human resources. Before converting its economy from agro-based to industry-based, it first worked on equipping its population with technical skills.

The unskilled workers were first put into the agro-sector, while vocational training was doled out to the rest of the population. Technical skills have become extremely vital for tech giants in countries like Japan, South Korea, and the West. China offered a good quality and skilled workforce at low rates, ultimately attracting all industries to the home base. Similarly, during the Wirtschaftswunder in Germany, the state already had a substantial population of highly skilled Germans, and regardless of the brain drain that took place during Operation Paperclip, Germany could industrialize its economy effortlessly.

Pakistan, too, must focus on this sector. We understand its significance due to our history. This is precisely why the 1950 5-year plan for industrialization of the economy collapsed—due to insufficient availability of technically skilled labor. One major impediment to Pakistan’s economy is the persistent energy crisis. Pakistan is heavily dependent upon imported fossil fuels, as thermal plants are responsible for 58.8% of its power generation. Similar trends are seen throughout the fiscal year, which has adverse effects on the trade deficit. Concurrently, the petroleum market is highly volatile, making the power sector extremely vulnerable to financial shocks.

These factors amalgamated have unpropitious ramifications for all economic sectors (agro, industrial, and services). The blackout earlier this year (2023) cost the textile industry a $70 million loss. Pakistan needs to take robust steps to tackle this menace to its economy. Investment is needed for existing power plants to be upgraded for better efficiency.

Furthermore, Pakistan must diversify its energy sector. The country was lucky enough to have a large indigenous gas supply. Unfortunately, due to mismanagement, heavy reliance upon fossil fuels, and irresponsible consumption, this supply has been depleted to critically low levels, so much so that now Pakistan has to fulfill 40% of its requirement from importing LNG.

Rather than relying heavily upon thermal plants, more heed must be given to other energy sources, especially alternative and renewable ones. Hydel (hydroelectric) power contributes 25.8%, nuclear 8.6%, and alternative power sources 6.8% to the national grid. Under the “ARE Policy 2020” (Alternative and Renewable Energy Policy) framework, Pakistan has taken an ambitious step to increase the contribution of alternative energy resources to 20% by 2025 and 30% by 2030. However, significant progress has yet to be made.

The ARE Policy 2020 did not highlight a complete, prudent, and incentivized regulatory framework. Additionally, it did not cater to the high initial costs of alternative technology that Pakistan is not yet ready to bear with the current state of pecuniary matters. Pakistan is also under a cascade of circular debt that accounts for almost Rs 2.31 trillion and needs to be addressed swiftly.

As mentioned earlier in this article, for growth in Pakistan, there is an urgent need for deep structural reforms. Opening up the economy to foster “ease of business” is imperative. The informal sector accounts for 35.6% of the GDP. This is a hefty amount of potential revenue that goes untapped mainly because people prefer to remain below the government’s radar, protecting themselves from stringent and inextricable rules and regulations, high business registration and renewal fees, and the intricate process of registering one’s business.

If you want to submit your articles and/or research papers, please check the Submissions page.

The views and opinions expressed in this article/paper are the author’s own and do not necessarily reflect the editorial position of Paradigm Shift.

Mr Hamza Sharif graduated with a degree in Mechanical Engineering from HITEC University. His areas of interest are geopolitics, current affairs, and history.