Pakistan-USA relations have been fluctuating significantly since the War on Terror era, indicated by fiery embraces or icy drifts during various time periods. These on-and-off relations can be attributed to Washington’s tilt towards India as a strategic partner in South Asia and Pakistan’s cordial relations with China. Under the Biden administration, Pakistan went through a period of relative diplomatic isolation. However, Trump’s 2.0 and post-2025 developments in Pakistan’s regional context have flipped the tables, with Pakistan emerging as the USA’s potential partner.

Besides this diplomatic shift, Trump’s 2.0 protectionist policies and trade war invoked China’s retaliatory export controls on rare earth elements, signalling the need for America to diversify its REE imports away from China. Rare earth metals power everything from electric vehicles and wind turbines to advanced missile guidance, stealth systems, and fibre-optic networks, all of which are lifelines for America’s protectionism. Pakistan’s critical minerals sector, constrained by tech dependency on China, offered a valuable source of supply to Trump’s America Great Again ambitions, thus repositioning Pakistan from a peripheral state to a central stakeholder in America’s Great Game against China. While Pakistan is maintaining, even exploring new avenues for strengthening its “all-weather friendship” with China, the underlying scepticism about China’s debt terms under CPEC and developmental returns from projects like Saindak has pushed Islamabad to hedge its bets – diversify its strategic partnerships.

Great Game for Critical Minerals: US and China as Cold Rivals

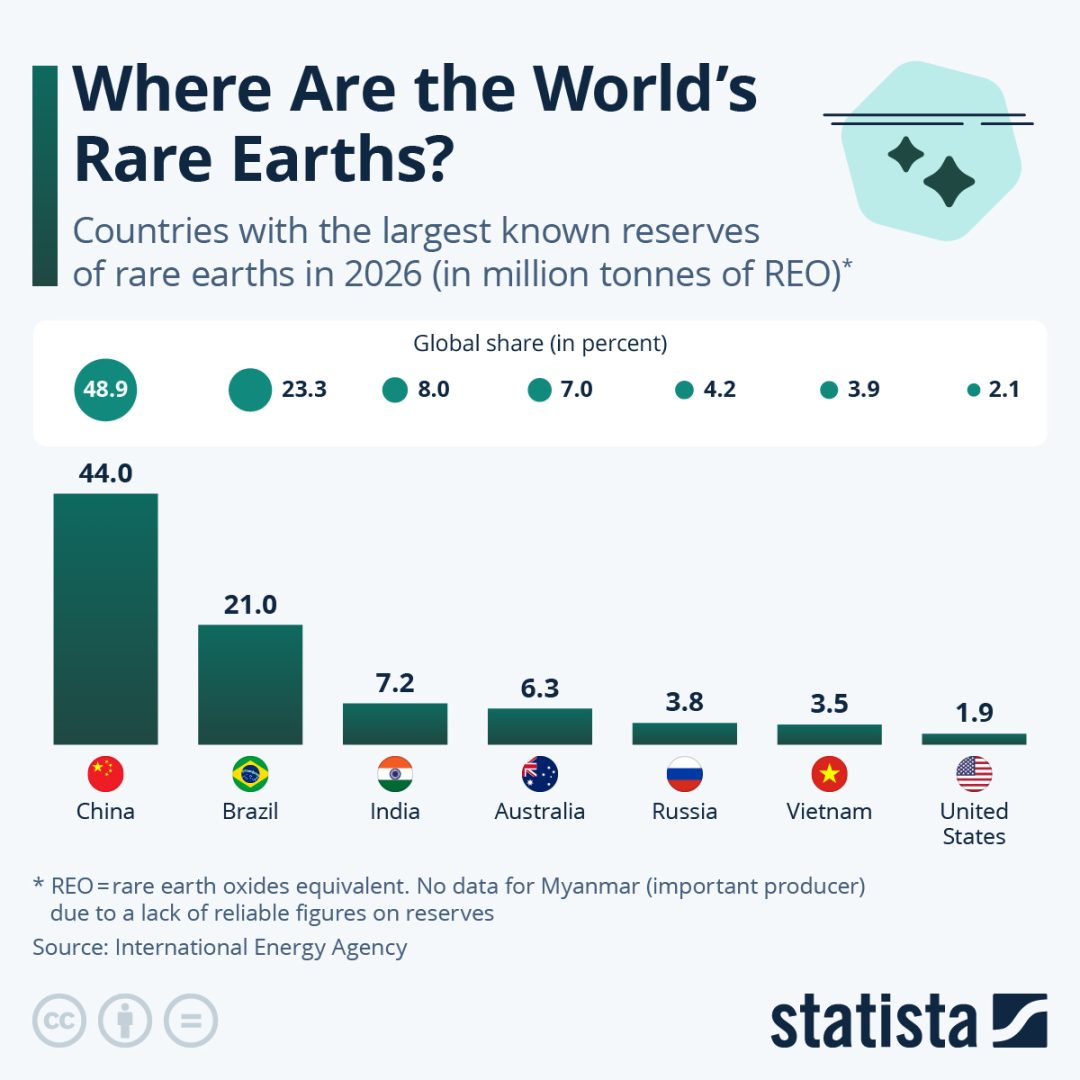

China holds a rare earth monopoly, as it controls approximately 70% of global rare earth mining and over 90% of global rare earth processing capacity, thus maintaining near-total domination of global supply chains. This monopoly has been enabled by decades of strategic state interventions and a whole-of-government approach, including the Communist Party, the state apparatus, the military complex, industry, and research institutions.

However, the stage for this dominance was set by the late Chinese leader, Deng Xiaoping, who noted, “The Middle East has oil. China has rare earths.” His pro-market reforms set the country on its path to becoming an economic powerhouse. Chinese strategy for gaining a monopoly over rare earth supply chains included subsidising domestic mining and processing, buying rare earth assets abroad, offering cheap exports to push foreign competitors out of business, centralising mining under state-owned enterprises, and tightening export quotas to increase geopolitical leverage.

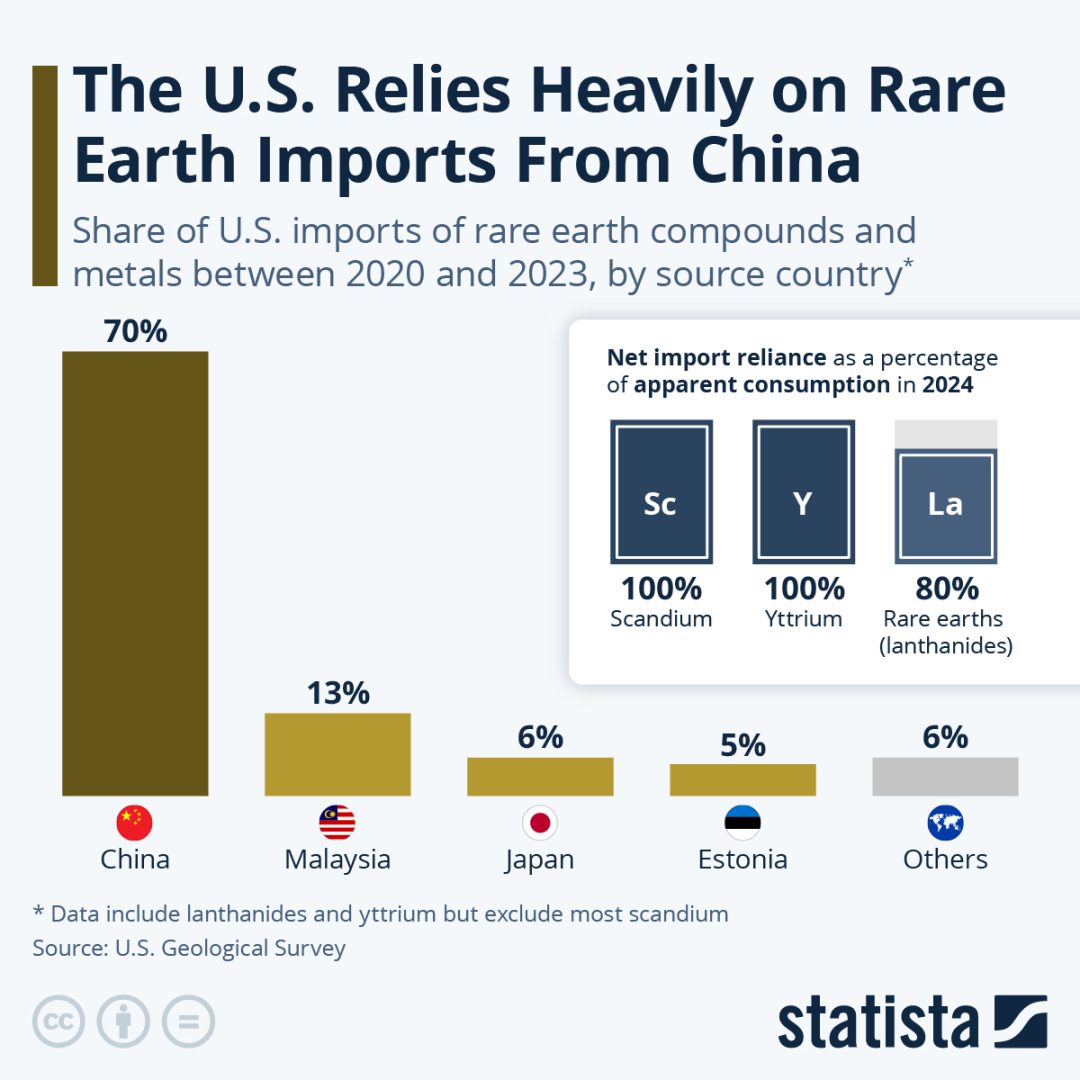

While China holds strategic dominance in REE processing, the USA holds a rare earth consuming monopoly (more than 80% of Western demands). The USA heavily relies on critical minerals and rare earths for development in both defence (F-35 avionics, missile guidance systems, and Golden Doom strategy) and commercial (electric vehicles, wind turbines, etc.) sectors, consuming ~12,000-15,000 tonnes of REO equivalent in 2024. The United States was the main global source of rare earth minerals, with Mountain Pass in California as the leading supplier, until the mid-1990s.

However, a combination of environmental constraints, corporate outsourcing, off-shoring polluting industries, and shortsighted government policies gradually dismantled the domestic supply chains. The major turning point that ended US dominance came in the 1990s, when US companies began offshoring rare earth processing to China, initially as a cost-saving measure and a way to avoid the Environmental Protection Agency’s (EPA) tightening regulations. Thus, China’s recent monopoly has also been subsidised by the West itself, or Beijing’s dominance is a self-inflicted wound from 1980s- 2000s globalisation.

However, the recent developments have pushed both the USA and China into a “Great Game over Critical Minerals and Rare Earth Elements”. For decades, the United States watched its manufacturing base erode as it chased low-cost labour overseas, easy access to raw materials, and the pursuit of environmental regulatory standards during the offshoring era of the 1990s and 2000s. Trump’s 2.0 reshoring movement and protectionist policies, which aimed at bringing manufacturing back to American soil, served national interests but triggered longer-term geopolitical and geo-economic repercussions.

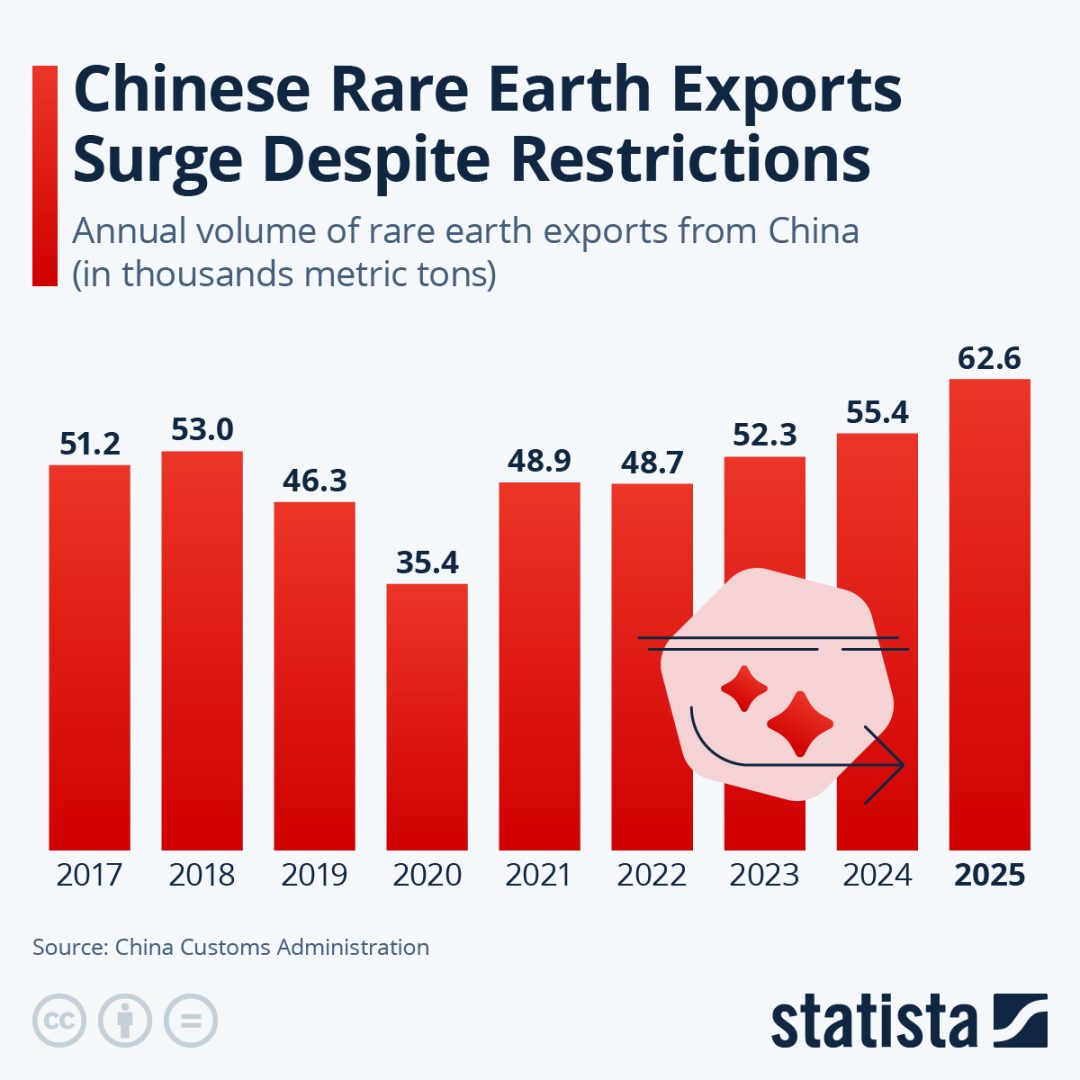

To narrow the USA’s trade deficit, President Donald Trump targeted top economic rivals, mainly China, with a cascade of tariffs on imports worth billions of dollars, launching a trade war. China retaliated by imposing export controls on rare earths, critical to Trump’s “Make America Great Again” (MAGA) ambition. Announcement No. 61 imposed extraterritorial control on rare earth materials, while Announcement No. 62 introduced restrictions on rare earth extraction and processing technologies, starting a deliberate war on rare earths. Though Beijing suspended the implementation of both announcements in November 2025, following a broader trade truce between China and the USA, this exposed the vulnerability of the USA’s supply chain dependence and accelerated Washington’s push for diversification.

USA, Pakistan & China: A Rare Earth Trinity

Beijing’s Announcement No. 61 hit America the hardest; F-35 magnets and Tesla NdPr choked overnight. Desperate to diversify its REE imports away from China, Washington discovered Pakistan, China’s ally in South Asia, jolting from the shocks of Announcement No. 62. Pakistan has a massive mineral potential, with world-class copper-gold deposits at Reko Diq and Saindak. Saindak is an old project run by Metallurgical Corporation of China under a long-term lease, producing around 20,000 tonnes of copper, 1.5 tonnes of gold, and 2.5 tonnes of silver each year.

China has extracted Saindak’s resources for nearly 15 years now on a long-term lease basis. However, Beijing’s cash cow, Saindak, after years of extraction, is now dead, and so are the developmental promises made. Balochistan, Pakistan’s province where Saindak is located, has benefited little from its enormously valuable resources, as the low-value minerals are extracted in Pakistan and exported to Chinese smelters for conversion into high-value end products. Pakistan’s lack of mainstream capacity, such as infrastructure and expertise for chemical separation, solvent extraction, and oxide-to-metal conversion, has facilitated this exploitation of its resources.

However, Saindak’s story is not an isolated case but a microcosm of a much broader structural failure associated with Pakistan-China relations through the China-Pakistan Economic Corridor (CPEC). Introduced as a development ladder for Pakistan’s collapsing energy sector and stagnating economy, CPEC, over time, has started to resemble a “financial trap.” According to the World Bank, China has become Pakistan’s single largest bilateral and commercial creditor, with Pakistan owing approximately $29 billion to China. Pakistan’s debt to China makes up nearly 30% of its total external debt.

Chinese bilateral deposits accounted for the largest share in Pakistan’s repayment of $22 billion of external debts in the 2025 fiscal year alone. Despite the soaring debts, the developmental returns for Pakistan’s economy are deeply asymmetrical. Saindak’s MCC operations have generated a revenue of $2.6 billion in foreign exchange between 2002 and 2022. However, Balochistan, the land that has provided the resources and paid the social and environmental costs, received a minimal share of 2%, which was later revised to 5%, of the overall revenue generation. Locals have also reported no visible development in the living standards or infrastructure.

Even after the 18th constitutional amendment, which delegated full authority to the provincial government over the management of natural resources, the federal government has blocked Balochistan government’s efforts to gain operational control of Saindak, citing the lack of technical capacity and development infrastructure. While it is framed as bureaucratic red tape, hindering Balochistan in achieving its constitutional rights, it is a self-fulfilling justification of how nearly two decades of Chinese operation involved no significant technology transfer. Therefore, now Pakistan’s efforts to diversify the strategic partnership in the critical mineral sector are less of a geopolitical gamble and more of an economically rational response to a partnership that has delivered dependence over development.

Reko Diq: Flipping the Script on America’s Critical Mineral Dilemma

The Reko Diq project can flip the script for both the U.S. and Pakistan. Pakistan formally entered the global critical mineral trade on October 2, 2025, sending its first consignment of enriched rare earths and critical minerals, containing antimony, copper concentrate, neodymium and praseodymium, to U.S. Strategic Metals (USSM) under a $500 million agreement. While the consignment was deeply symbolic, as Pakistan currently lacks industrial infrastructure for REE extraction and processing, it established a political framework for deeper cooperation. Antimony diversification for Washington addresses a glaring supply-chain vulnerability, as the metal is integral to ammunition primers, flame-retardant compounds and other advanced electronics.

For Pakistan, antimony represents a credible near-term export opportunity and a path to earn strategic credibility while REE development proceeds. Copper represents another indispensable material in modern defence production, forming part of almost every element of the military industrial base, from power systems and communications to weapons platforms and infrastructure. Thus, copper forms the backbone of U.S. defence capability, and any disruption to its supply or processing capacity carries strategic consequences.

While China controls over half of global smelting, Pakistan’s copper concentrates at Reko Diq provide incremental diversification for Washington, which accounts for just 5% of global production and 3.3% of refining capacity. These estimated Reko Diq reserves, among the largest undeveloped copper and gold deposits in the world, represent a long-term anchor for this Pak-USA strategic partnership. However, China’s Announcement No. 62, made on October 9, 2025, and suspended later on in November following the trade truce, signalled Beijing’s intent to restrict the technology transfers. China’s retaliatory response to the USA served as a warning shot for Pakistan as well, signalling a threat to Pakistan’s ambition to develop domestic processing capabilities, export value-added minerals to the United States, and diversify its critical minerals supply chains.

Pakistan’s Next Move

China overplayed its monopoly hand, with announcements 61 and 62, before a partial retreat in November, and exposed a structural vulnerability that neither Washington nor Islamabad can afford to ignore. This also revealed that America’s dependency on Chinese processing and Pakistan’s reliance on China’s extraction technologies are strategic liabilities and not just economic inconveniences. From this shared vulnerability, a strategic partnership between the two begins to take shape.

The United States has partnerships and critical minerals deals with Japan and Australia. But most of these deals are focused on developing rare earth processing technologies and building joint supply chains through joint financing mechanisms and stockpiling systems. However, these Japan-USA & USA-Australia partnerships, while significant, are constrained by the limited scale of new untapped resources. Pakistan’s estimated $6T mineral jackpot, a figure drawn from Pakistan’s geological survey, while contested by independent analysts, offers a resource base of genuine strategic significance.

Japan, like the USA, depended on China for most of its rare earth imports until 2010, when a diplomatic dispute between the two led China to impose export controls on rare earths. Japan responded with unusual urgency, deploying more than $1.1 billion to diversify supply chains, invest in overseas mining and processing projects, support domestic recycling and help manufacturers redesign components to use fewer rare-earth elements. Central to Japan’s long-term resilience was its partnership with Lynas Rare Earths in Australia. This partnership created the only significant non-Chinese rare-earth separation capacity in the world, showing that diversification is possible. Recent critical mineral deals with the United States have added to the significance of this partnership.

Pakistan’s immediate entry point into this supply chain is shipping Balochistan’s raw critical mineral concentrates to the USA and its critical mineral bloc, a near-term revenue generation stream while domestic industrial, processing, and technological infrastructure is built. This should not be taken as a permanent position where Pakistan is once again made a raw material supplier, but as a deliberate first phase mirroring Japan’s own trajectory after 2010, when it first diversified sourcing before building domestic industrial capacities.

The second major step in Pakistan’s strategy that can add value at home is “technology transfer” from the American bloc, supported by the USA’s Export-Import Bank (EXIM) financing to Pakistan. This will not only reduce Pakistan’s technological dependence on Chinese extraction and processing systems but also create jobs for locals in Balochistan, directly addressing the asymmetry that Chinese extraction partnerships never resolved. Thirdly, the construction of Pasni Port could significantly alter regional trade and energy dynamics. Pasni sits in the province of Balochistan, which borders Afghanistan and Iran, between the Strait of Hormuz, Central Asia, and the Balochistan mineral belt. Whoever controls this coastline will influence energy, trade, and data routes of the next decade. Pakistan has pitched an idea of a new deep-sea port at Pasni to Washington, which, if materialised, could reshape China’s strategic dominance over regional trade routes.

Conclusion: The Long Game of Critical Minerals

The window for this “strategic partnership” is real but narrow. China’s suspension of announcements 61 and 62 was tactical and not structural. Beijing still holds a monopoly over rare earth reserves, and its extraction and processing technology leverage is still intact. For Washington, Pakistan is no longer a peripheral state that needs to be managed through a security-development or counter-terrorism nexus but a potential node in critical mineral architecture that America desperately wants to build and develop.

For Islamabad, this minerals pivot represents an exit ramp from decades of dependence and an opportunity to diversify its partnerships in an evolving international political environment. However, one thing that needs to be clear from the outset is that this is a “long-term game”, rather than a short-term venture ensuring quick revenue generation. If Pakistan can hold its nerve, invest in processing capacity, and deliver its supply commitments, it will not only be a mere raw material exporter to a powerful patron but also a strategic node in global critical minerals supply chains. Pakistan’s critical mineral bet can earn it a seat at the table of the next industrial order, one where whoever controls the inputs to clean energy and advanced defence will shape the century or theoretically “rule the world”. Pakistan has the minerals. The question is whether it has the institutions, security, and resolve to stay in the match long enough to have all the cards in its court.

If you want to submit your articles and/or research papers, please visit the Submissions page.

To stay updated with the latest jobs, CSS news, internships, scholarships, and current affairs articles, join our Community Forum!

The views and opinions expressed in this article/paper are the author’s own and do not necessarily reflect the editorial position of Paradigm Shift.

Javeria Abbas is an International Relations student with a deep interest in global governance, development economics, and climate policy. Her work focuses on examining contemporary global challenges through the lenses of sustainability, international cooperation, and equitable development. She is passionate about research, policy analysis, and amplifying perspectives from the Global South on issues shaping the international system.